A Deeper Dive - How One Apartment Complex's Loan Explains a National Housing Crisis

Renters’ lives are often tied to financial systems designed to prioritize profit over stability. It’s a sobering reality—and one that lies at the heart of the American housing crisis. The story of the Chadwick Apartments in Los Angeles provides a compelling window into this complex issue. Let’s explore how multi-million-dollar loans, intricate financial instruments, and the aspirations of everyday renters intersect.

The Anatomy of a Risky Loan

Imagine finding your dream home but having to sign a contract so dense it feels impenetrable. Now imagine scaling that complexity up to a $58.6 million loan, the size of the one Tides Equities took out for the Chadwick Apartments. Why does this loan matter? Because it illustrates the fragility of a system that underpins housing for millions of Americans.

Tides Equities, known for acquiring properties with potential for rent increases, grew its portfolio to over 31,500 units. The Chadwick Apartments were a part of this expansion. However, the loan secured for the acquisition wasn’t just any loan—it was tied to the mortgage-backed securities (MBS) market. Sound familiar? This was the same mechanism at the center of the 2008 financial crisis, where risky loans were bundled and sold to investors, fueling widespread instability.

Housing as a Balancing Act

As Professor David Reiss from Brooklyn Law School explains, housing policy must balance three principles: treating housing as an economic good, respecting it as a human right, and recognizing it as a foundation of democratic stability. Yet, these principles often collide in a market driven by profit.

This balancing act is reflected in the Chadwick Apartments’ story. As Tides Equities faced challenges repaying the loan, the potential repercussions for tenants loomed large. Foreclosure or default often prompts rent hikes, forced sales, or even evictions—all outcomes that destabilize lives.

The Bigger Picture: A Nationwide Crisis

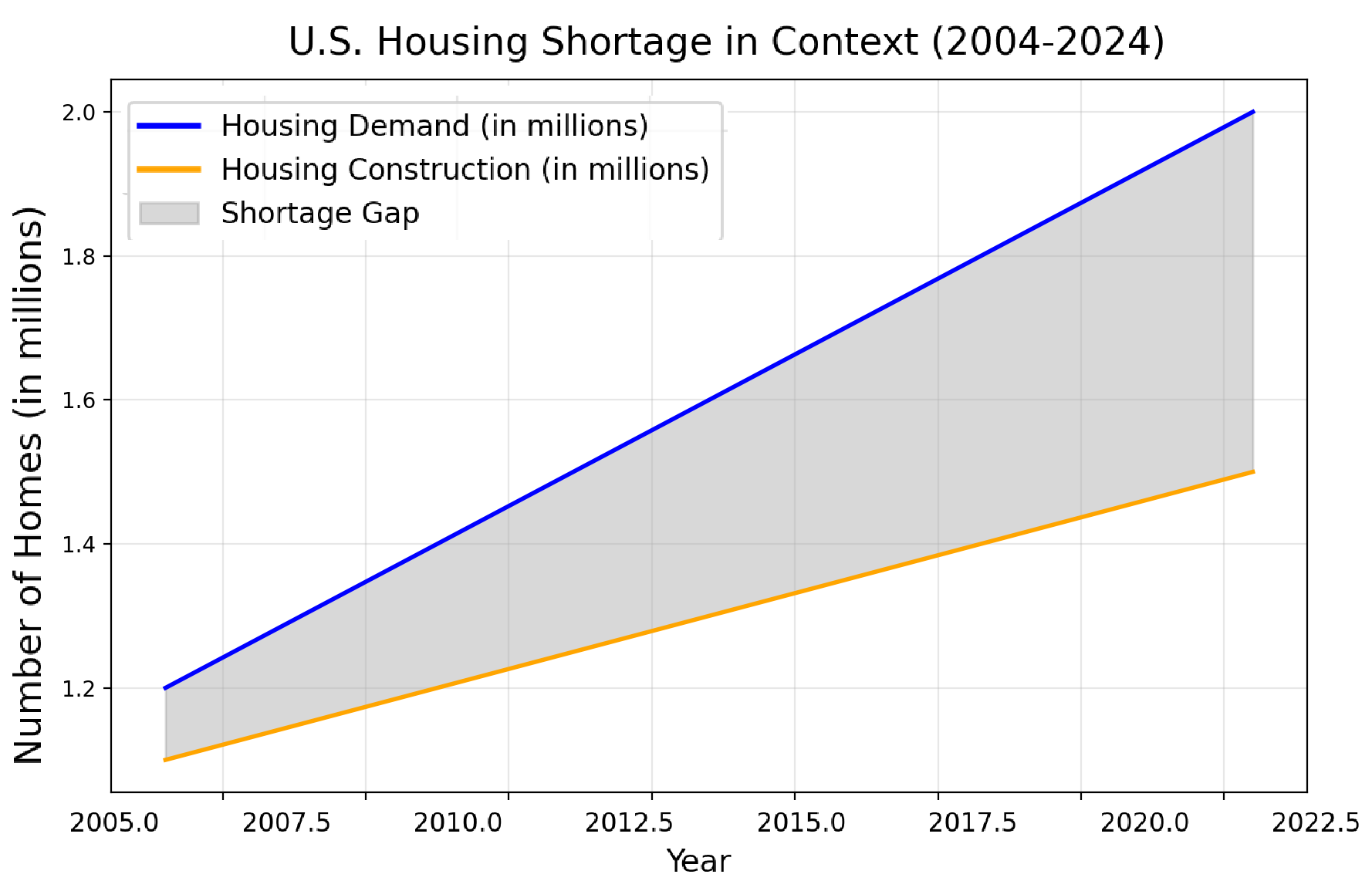

The struggles at Chadwick are not an isolated case. Across the United States, the housing shortage currently stands at approximately 3.7 million units. This means that there are 3.7 million fewer homes available than needed to meet demand.

The shortage arises from several factors, including insufficient housing construction over the past decade, rising construction costs, and restrictive zoning laws. This gap affects renters and prospective homeowners alike, driving up housing costs and making affordable living increasingly out of reach.

Visual Insight: U.S. Housing Shortage in Context

To help put this into perspective, the graph below compares the demand for housing with the actual number of homes constructed over the past two decades. Notice how the gap between what’s needed and what’s available has grown.

Learning from History: 2008 and Beyond

The parallels to the 2008 financial crisis are striking. High-risk lending practices, tied to speculative investments, led to global economic turmoil. While regulatory reforms emerged from that crisis, today’s housing challenges reveal gaps in enforcement and oversight.

The takeaway? Without robust safeguards, housing stability remains elusive. The Chadwick Apartments’ story underscores the need for policies that prioritize tenants over investors. Solutions such as stronger tenant protections, incentives for affordable housing, and regulation of speculative practices are crucial for breaking the cycle.

A Call for Action

For American renters, the message is clear: homes should be more than investments—they should be foundations for life and community. Addressing the housing crisis requires more than market-driven solutions. It demands a commitment to balancing economic goals with human needs. Because at the end of the day, stability in housing isn’t just about finance—it’s about fairness.